Table of contents:

- Cash In Life Insurance Policy: A Comprehensive Guide

-

FAQ about Cash in Life Insurance Policy

- What is cash in a life insurance policy?

- How does cash value work?

- When can I access the cash value?

- What are the benefits of having cash value?

- What are the risks of cash value?

- How do I choose the right cash value policy?

- What happens to the cash value when I die?

- Can I add cash value to an existing policy?

- Can I use the cash value to pay for premiums?

Cash In Life Insurance Policy: A Comprehensive Guide

Introduction

Readers, are you looking for ways to leverage your life insurance policy to meet your financial needs? Consider "cashing in" your policy. This option allows you to access the policy’s cash value while you’re still alive. In this article, we’ll explore the ins and outs of cashing in a life insurance policy, so you can make informed decisions about your financial future.

How Cash Value Life Insurance Works

Cash value life insurance policies are a hybrid of life insurance and savings. A portion of your premiums goes towards a cash value account that grows over time. This account earns interest, and you can borrow against it or withdraw funds as needed. As long as the policy is in force, the death benefit remains intact.

When to Cash In Your Policy

There are several reasons why you might consider cashing in your life insurance policy:

- Unexpected Expenses: If you face a financial emergency, cashing in your policy can provide quick access to funds.

- Supplementing Retirement: The cash value can be used to supplement your retirement income or cover unexpected healthcare expenses.

- Estate Planning: If you have other assets to leave to your beneficiaries, you may choose to cash in your policy to reduce estate taxes.

Cash Value Withdrawals and Loans

When you cash in your policy, you can choose between two options:

- Withdrawals: Withdrawals reduce the death benefit and cash value of the policy. You may have to pay income taxes on withdrawn funds.

- Loans: Loans do not reduce the death benefit, but they must be repaid with interest. If the loan is not repaid, the policy may lapse.

Pros and Cons of Cashing In

Pros:

- Access to funds when needed

- Potential for tax-free growth (for withdrawals within certain limits)

- Can supplement retirement income or cover expenses

Cons:

- Reduces death benefit

- Potential for income tax on withdrawals

- If not managed properly, the policy may lapse

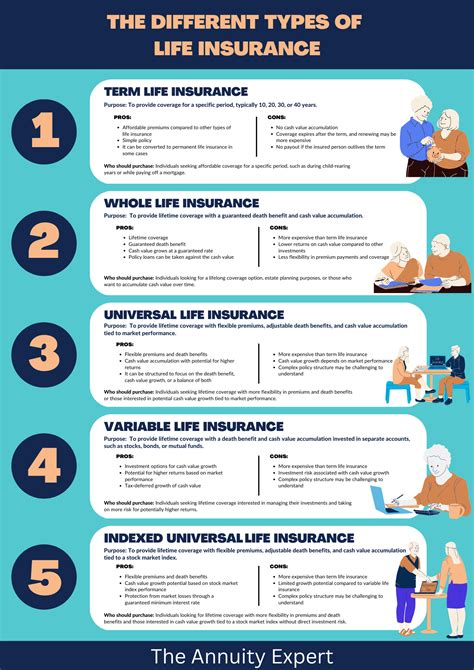

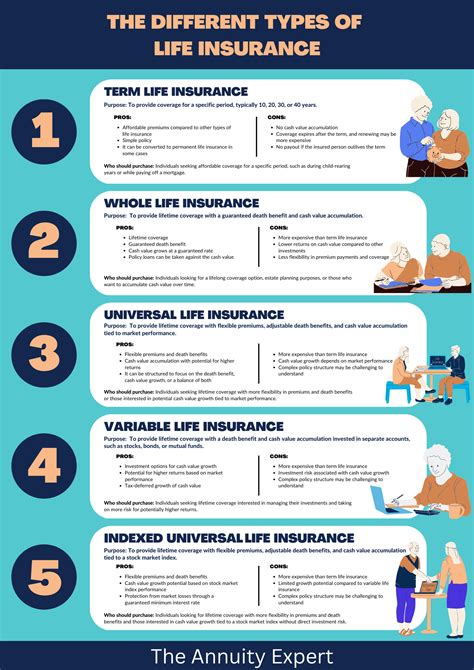

Cash Value Life Insurance Policy Options

There are different types of cash value life insurance policies available:

- Whole Life Insurance: Policies with a fixed death benefit and cash value that grows over time.

- Universal Life Insurance: Policies with a flexible death benefit and cash value that may fluctuate based on performance.

- Variable Life Insurance: Policies with a death benefit and cash value that are linked to the performance of a stock or bond index.

Table: Cash Value Life Insurance Policy Options

| Policy Type | Death Benefit | Cash Value | Flexibility |

|---|---|---|---|

| Whole Life | Fixed | Guaranteed to grow | Low |

| Universal Life | Flexible | May fluctuate | Moderate |

| Variable Life | Tied to market performance | May fluctuate | High |

Conclusion

Cashing in a life insurance policy can be a valuable tool if you need access to funds or want to supplement your retirement income. However, it’s crucial to weigh the pros and cons carefully and choose the policy that best meets your individual needs. Remember to explore other articles on our website for more information on life insurance and financial planning.

FAQ about Cash in Life Insurance Policy

What is cash in a life insurance policy?

- The cash value is a fund that accumulates within your policy. You can borrow against it or withdraw it, but doing so will reduce the death benefit.

How does cash value work?

- A portion of your premium payments goes towards building up the cash value. Over time, the cash value grows through interest and dividends.

When can I access the cash value?

- You can typically withdraw or borrow against the cash value after a few years, depending on your policy. Some policies may limit withdrawals or loans until the policy is fully paid up.

What are the benefits of having cash value?

- It can provide you with a source of emergency funds without having to surrender the policy.

- It can supplement your retirement savings.

- It can help you cover unexpected expenses.

What are the risks of cash value?

- If you withdraw or borrow too much from the policy, it can reduce the death benefit.

- The cash value may not grow as quickly as you hoped, especially in the early years of the policy.

- If you surrender the policy before it has built up a significant cash value, you may lose money.

How do I choose the right cash value policy?

- Consider your financial goals and needs.

- Compare different policies to find one that suits you best.

- Talk to an insurance agent for professional advice.

What happens to the cash value when I die?

- The death benefit is paid to your beneficiaries, regardless of the cash value.

- If there is any remaining cash value, it is typically distributed to your beneficiaries along with the death benefit.

Can I add cash value to an existing policy?

- In some cases, you may be able to add a cash value rider to an existing term life insurance policy.

- Check with your insurance company to see if this option is available.

Can I use the cash value to pay for premiums?

- Yes, you can use the cash value to pay for your premiums, but this will reduce the cash value and the death benefit.

- It’s generally not recommended to use the cash value to pay for premiums unless you have no other options.