Table of contents:

-

FAQ about Car Insurance in Montana

- 1. What are the minimum car insurance requirements in Montana?

- 2. Is uninsured motorist coverage required in Montana?

- 3. What are the penalties for driving without insurance in Montana?

- 4. How much does car insurance cost in Montana?

- 5. What factors affect car insurance rates?

- 6. What is a deductible?

- 7. What is comprehensive coverage?

- 8. What is collision coverage?

- 9. How can I get a lower car insurance premium?

- 10. What should I do if I get into an accident in Montana?

# Avoiding Costly Montana Road Surprises: A Comprehensive Guide to Car Insurance in Montana

## Hey Readers: Navigating Montana’s Car Insurance Landscape

Montana’s stunning landscapes, vast expanses, and picturesque roads beckon travelers and residents alike. However, understanding and securing adequate car insurance in Montana is paramount to avoid costly surprises and ensure peace of mind during your journey. This article aims to provide a comprehensive overview of Montana’s car insurance landscape, equipping you with the knowledge to make informed decisions and protect yourself financially on the road.

## Unraveling Montana’s Car Insurance Requirements

### Legal Minimum Coverage

Like most states, Montana mandates drivers to carry minimum liability insurance coverage, providing essential protection against damages or injuries caused to others. The required coverage amounts are:

– Bodily injury liability: $25,000 per person, $50,000 per accident

– Property damage liability: $15,000 per accident

### Recommended Coverage

While meeting the legal minimum is essential, it may not fully shield you from financial risks. Consider additional coverage options to enhance your protection:

– Collision and comprehensive coverage: Protects your vehicle from damage or loss due to accidents, theft, or natural disasters

– Uninsured/underinsured motorist coverage: Provides protection if you’re involved in an accident with a driver who lacks insurance or has insufficient coverage

– Medical payments coverage: Covers medical expenses for you and your passengers, regardless of fault

## Understanding Montana’s Car Insurance Costs

### Factors Affecting Rates

Numerous factors influence car insurance rates in Montana, including:

– Driving history: Safe driving records lead to lower premiums

– Vehicle type: Sports cars and luxury vehicles generally cost more to insure

– Age and experience: Younger drivers and those with less experience pay higher rates

– Location: Rates vary depending on your city or county

– Coverage limits: Higher coverage amounts result in increased premiums

### Ways to Save

Exploring ways to lower car insurance costs in Montana can save you significant money. Consider:

– Comparison shopping: Obtain quotes from multiple insurance companies to compare premiums

– Maintaining a good driving record: Avoid traffic violations and accidents

– Increasing your deductible: Choosing a higher deductible lowers your premiums

– Bundling policies: Combining car and home insurance can provide discounts

– Taking defensive driving courses: Some insurers offer discounts for completing these courses

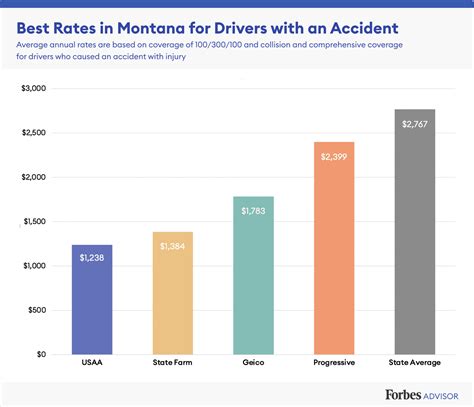

## Montana Car Insurance Companies: A Comparative Overview

### Top-Rated Insurers

Montana’s car insurance market offers a wide range of providers. Here are a few highly rated insurers:

– State Farm

– AAA

– Progressive

– Farmers

– Allstate

### Insurance Comparison Table

To help you make an informed decision, we’ve compiled a table comparing key aspects of these top insurers:

| Company | Average Premium | Customer Satisfaction | Financial Stability |

|—|—|—|—|

| State Farm | $600-$1,200 | Excellent | Very good |

| AAA | $700-$1,400 | Good | Excellent |

| Progressive | $500-$1,100 | Very good | Good |

| Farmers | $650-$1,300 | Good | Excellent |

| Allstate | $750-$1,500 | Fair | Very good |

## Practical Tips for Montana Drivers

### Montana Car Insurance Laws and Regulations

– Montana follows a comparative negligence system, meaning fault is assigned to each driver involved in an accident.

– Montana has a six-year statute of limitations for filing insurance claims.

– Drivers involved in accidents with property damage over $1,000 must report them to the Montana Highway Patrol.

### Preparing for Insurance Claims

– Document the accident scene, including photos and witness contact information.

– Report the accident to your insurer promptly.

– Cooperate with the insurance adjuster and provide all requested information.

## Conclusion: Embracing Montana’s Roads with Confidence

Understanding and securing adequate car insurance in Montana is crucial for both legal compliance and financial protection. By navigating the requirements, understanding the costs, comparing insurance companies, and following practical tips, you can ensure peace of mind while embracing the beauty of Montana’s roads.

For further insights and valuable tips on a wide range of topics, be sure to explore our other articles. Stay informed and navigate life’s challenges with confidence!

FAQ about Car Insurance in Montana

1. What are the minimum car insurance requirements in Montana?

- Liability coverage: $25,000 per person and $50,000 per accident for bodily injury.

- Property damage liability coverage: $15,000 per accident.

2. Is uninsured motorist coverage required in Montana?

- No, but it is highly recommended.

3. What are the penalties for driving without insurance in Montana?

- Fines ranging from $350 to $1,000.

- License suspension for up to six months.

4. How much does car insurance cost in Montana?

- Rates vary depending on factors such as age, driving history, and vehicle type. However, Montana has some of the lowest insurance rates in the country.

5. What factors affect car insurance rates?

- Driving history

- Age

- Vehicle type

- Location

- Credit score

6. What is a deductible?

- The amount you pay out-of-pocket before insurance coverage begins. A higher deductible typically lowers your premiums.

7. What is comprehensive coverage?

- Coverage that protects your car from events other than collisions, such as theft, vandalism, and weather damage.

8. What is collision coverage?

- Coverage that pays for damage to your car in the event of a collision with another vehicle or object.

9. How can I get a lower car insurance premium?

- Maintain a good driving history.

- Increase your deductible.

- Take a defensive driving course.

- Bundle your car insurance with other policies, such as renters or homeowners insurance.

10. What should I do if I get into an accident in Montana?

- Stay calm and check for injuries.

- Call the police and report the accident.

- Exchange information with the other driver(s) involved.

- Contact your insurance company as soon as possible.